Buying a House vs. Renting: A Lifestyle Choice

There comes a time in life when everyone has to consider their living situation: Do you continue to rent, or do you take the plunge and buy a house? Or more precisely, when should you buy a house versus rent?

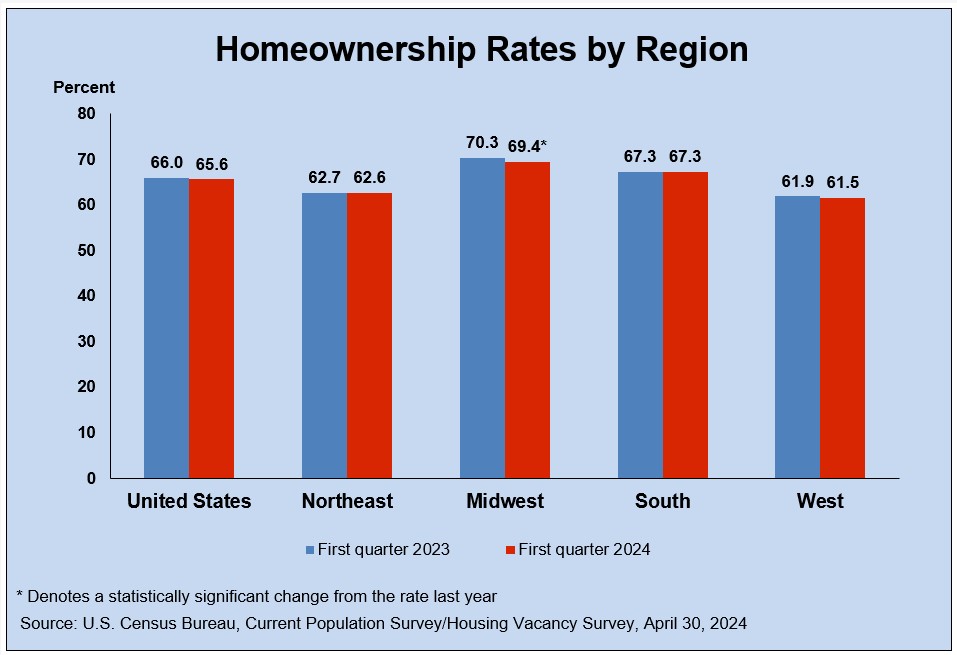

Sure, two-thirds or Americans are homeowners, according to the most recent U.S. Census. But rising interest rates and low housing inventory might have some people wondering if they should continue to rent, just for a little longer.

{kind=link}

Here at Select Properties, we are big on the prospect of owning your own home. The difference between buying a house and renting is similar to setting up a temporary container garden on a patio vs. planting a beautiful garden in the ground with flowers that return and bloom year after year. Homeowning is about permanence, expressing your personal style, and the chance to build generational wealth.

Sure, renters enjoy a certain freedom from responsibility. But that is because renting is more transitory—which may or may not be what you are looking for.

So, if you’re on the fence about which way to go, consider how your decision to either rent or buy will impact your lifestyle. Here’s how to do that.

Buying a House vs. Renting: The Big Picture

Imagine how you would feel, driving up to your new home after the close. Think of all the possibilities you envision for painting, decorating, landscaping, and entertaining in a space that’s uniquely your own. For the first time, as a new home owner, there’s no landlord to answer to because you’re making an investment into your own future. In essence, you’re betting on yourself to succeed.

There’s freedom in knowing that you always have an asset that you can count on. After all the hard work you’ve done to boost your credit score, save for a down payment, and qualify for a mortgage, owning a home offers a big return on your investment. Most importantly, a home allows you the freedom to put down roots for generations to come.

On the other hand, renters, too, can feel attached to their homes, condos, or apartments. There are benefits to renting, especially for young people. Renters can:

- Move often and travel worry-free.

- Save more money without home repair, mortgage, or other ownership costs.

- Eat out more frequently and play more often.

- Expect the owner to make all repairs.

- Meet other renters with similar interests and lifestyles.

The downside is that, even with perks like on-site gyms, swimming pools, and clubhouses, as a renter, you basically pay just for a roof over your head (and maybe a parking space). There are no financial incentives to benefit you at tax time.

If you’re tired of paying rent and you are weighing buying a home vs renting, a rent vs buy calculator permits you to take your lifestyle into consideration. This tool allows you to:

- input information on your location, approximate home price, whether you use a fluctuating or fixed mortgage (a 30-year is the norm) and how much rents cost in the area.

- compare the costs of buying against the costs of renting for a specific period of time.

- compare upfront costs for a home such as the down payment, appraisal, mortgage insurance, earnest money, application fees, and closing vs costs for renting, like a security deposit and renter’s insurance.

So, when should you buy a house? The answer is simple: Buy when you feel the time is right!

Buying a Home for the First Time is Emotional

There’s a certain emotional stability in buying a home. We often hear about the stress of homeownership but the payoff is not only financial in terms of building generational wealth, but homeownership creates warm memories to last a lifetime. This is why the idea of having a home pushes so many emotional buttons.

Buying a home allows a freedom of expression that is not always available to the renter. Homeownership gives us the chance to create a safe space that shouts out our individuality. Painting the home office flaming red or the kitchen robin’s egg blue allows us to be free and unique. That’s why buying a home remains the Gold Standard for Americans.

Deciding on the choice of renting or buying involves taking stock of your lifestyle today and how you envision living tomorrow. With buying a home, your mortgage basically stays the same for the life of the loan. Renting, unlike buying, leaves renters with more unknowns when it comes down to the whims of a changing housing market or a neighborhood, and how high and how fast your rent can increase.

Renting vs. buying reflects a personal choice, but consider the plus and minuses of buying a home for the first time:

- Freedom from answering to a landlord on your creative choices as a homeowner. You have the freedom to remodel, add a swimming pool, hot tub, or sauna. When you rent, can you even add floating shelves for your books? Renting doesn’t allow you to add a privacy fence to your backyard or build out your den.

- Renting allows you to travel when, where, and how often you like because you’re not paying property taxes, replacing appliances, or shelling out for a new roof. On the flip side, buying a home helps you to build equity—producing money for a bigger home purchase or creating a safety net to give you peace of mind. Plus, you benefit from certain tax incentives as a first time home buyer.

- Buying a home enhances your stability but you may miss out, at least in the beginning, on having the renter’s carefree lifestyle to buy a new car or take that cruise in the off season. Still, unlike a car or a vacation, a home appreciates in value. Doing things to improve your property with exterior lighting, an enclosed porch, and planting a vegetable garden pays off in dividends for the future.

Deciding to Become a First Time Home Buyer

If you've decided to become a first time home buyer, congratulations! Buying a house for the first time is a major life decision. Stability is key. If you have a steady income and you pay your bills on time, you can buy a house on your own or if you’re in a solid relationship. (Two incomes will make you an even better mortgage candidate.)

Although the 20% down payment has always been the norm, there’s additional help for first time home buyers with down payment assistance as low as 3%, depending on the program. Whether you’re a teacher, a firefighter, or police officer, there are grant programs that don’t require repayment. There are even programs that will qualify you for a home if you’re low or middle income.

Cover Image by photobyphotoboy purchased on Envato Elements

Share This Post

| Previous Post | Next Post |